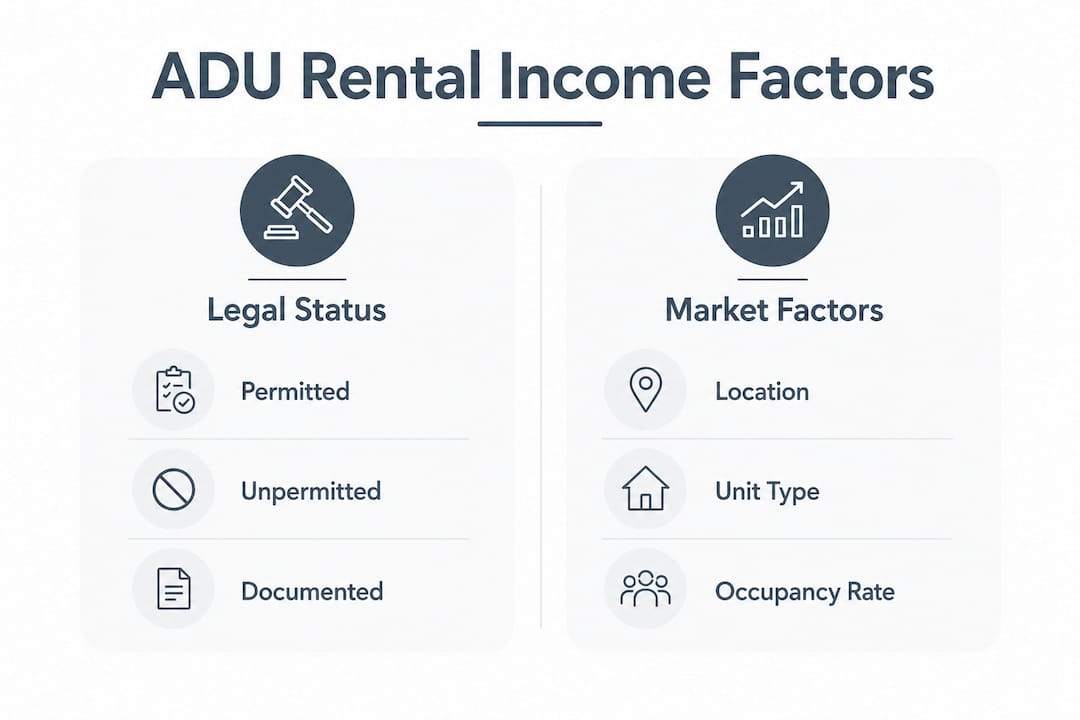

ADU rental income potential is defined as the gross rent an accessory dwelling unit generates, measured against the financing rules, legal requirements, and market conditions that determine how much of that rent you can actually use. A well-positioned ADU can generate meaningful monthly cash flow, but Fannie Mae’s 2026 underwriting rules cap the qualifying portion at 30% of total qualifying income, which changes how you model the numbers before you ever talk to a lender. Understanding both the income side and the regulatory side is what separates a profitable ADU from an expensive surprise.

How is ADU rental income calculated and used in mortgage qualification?

ADU rental income enters the mortgage qualification process through a specific formula, not a simple rent-to-income ratio. Under Fannie Mae’s Desktop Underwriter v12.1, effective March 21, 2026, ADU rent counts toward qualifying income for a one-unit principal residence on both purchase and limited cash-out refinance transactions. The 30% cap is the critical constraint. If your total qualifying income is $10,000 per month, no more than $3,000 of that can come from ADU rent, regardless of what the unit actually earns.

Only one ADU’s rental income counts toward qualification, even if the property has more than one accessory unit. That rule matters for investors who build multiple units expecting to stack rental income for financing purposes. Lenders will not count the second unit’s rent in the qualifying calculation.

Documentation requirements are strict. Lenders typically require a signed lease agreement, evidence of rental history if available, and an appraisal that supports the rental income figure. The appraiser must confirm that the rent claimed is consistent with the local market.

- 30% cap: ADU rent cannot exceed 30% of total qualifying income under Fannie Mae’s DU v12.1 rules.

- One unit only: Only one ADU’s rent counts, even on multi-unit properties.

- Lease required: A signed lease agreement is standard documentation for lender acceptance.

- Appraisal support: The appraiser must confirm the rent is market-consistent.

- Purchase and refinance: The rule applies to both transaction types, not just purchases.

Pro Tip: Run your qualifying income calculation before you assume ADU rent will cover a significant portion of your mortgage payment. The 30% cap often surprises homeowners who expected to count the full rent.

The practical effect is real. A borrower earning $8,000 per month in W-2 income with an ADU renting for $1,500 per month can count only $2,400 of ADU rent at most, since 30% of $9,500 total is $2,850, and the actual rent of $1,500 falls under that ceiling. In this case, the full $1,500 counts. But a borrower with lower base income hits the cap faster. Knowing your ceiling before applying saves time and avoids rejected applications.

What role do ADU legal status and comparables play in rental income potential?

Legal permitting is the foundation of ADU rental income viability. An unpermitted ADU generates rent in practice, but that income is invisible to lenders and appraisers. Income from illegal ADUs is not eligible for lender-supported appraisal or financing. That means you cannot use it to qualify for a mortgage, and the unit’s value contribution to the property is limited.

Freddie Mac’s ADU fact sheet requires that rental income be supported by at least three comparable rentals, including at least one with a rented ADU. That standard exists because ADU rents behave differently from standard apartment rents. A comparable must reflect the same privacy level, unit type, and general location. Using apartment comps for a detached backyard studio will overstate achievable rent and create appraisal problems.

- Confirm legal permitting. Verify the ADU has a certificate of occupancy and is recorded as a legal dwelling unit with the local jurisdiction.

- Pull ADU-specific comps. Find at least three comparable rentals in your area, with at least one being a rented ADU of similar size and type.

- Match unit characteristics. Comps must reflect the same privacy level, bedroom count, and general location as your unit.

- Engage a qualified appraiser. Use an appraiser experienced with ADU valuations, not a standard residential appraiser unfamiliar with accessory unit income.

- Document everything. Keep permits, inspection records, and lease history in a single file for lender review.

Pro Tip: If you are buying a property with an existing ADU, ask the seller for the permit history before closing. An unpermitted unit that looks rentable on paper can cost you months of legalization work and thousands in retrofitting.

Legal compliance also affects long-term rental stability. A permitted ADU can be listed on rental platforms, advertised openly, and defended in court if a tenant dispute arises. An unpermitted unit puts you in a legally vulnerable position on every front. The ADU legal permitting process is worth completing before you count a single dollar of rental income.

What rental income can you expect from ADUs in typical markets?

Market rent for ADUs varies significantly by location, unit type, and finish level. A concrete benchmark comes from Fresno County, where a typical 1-bedroom ADU rents for $1,323 per month with a 96% occupancy rate. That occupancy rate implies roughly $15,241 in gross annual rent and supports a 6.5% cap rate on a well-priced unit.

| Market factor | Fresno County example | General implication |

|---|---|---|

| Monthly rent | $1,323 | Baseline for 1-bedroom ADU |

| Occupancy rate | 96% | Strong demand, low vacancy |

| Gross annual rent | ~$15,241 | Before expenses and vacancy reserve |

| Cap rate | 6.5% | Solid return for a secondary unit |

Cap rate measures net operating income divided by property value. A 6.5% cap rate on an ADU means the unit generates $6.50 in net income for every $100 of its assessed value. That is a meaningful return, especially when the ADU sits on land you already own.

Several factors push rent higher or lower than the market average:

- Unit type: Detached ADUs with private entrances command higher rents than attached or garage-conversion units.

- Finish level: Stainless appliances, in-unit laundry, and updated bathrooms increase achievable rent. The impact of amenities on rent is well-documented in ADU markets.

- Location within the market: Proximity to employment centers, transit, and schools drives demand.

- Floor plan efficiency: A well-designed 400-square-foot studio with smart storage rents closer to a 500-square-foot unit with poor layout. Efficient ADU floor plans directly affect rental appeal.

Modeling rental income conservatively means using 90–95% occupancy rather than 100%, and budgeting for one month of vacancy per year. That discipline produces realistic projections and avoids the trap of assuming best-case rent every month of the year.

How do lease terms and rental management practices affect realized ADU income?

A signed lease agreement is the single most effective tool for protecting ADU rental income. California ADU lease agreements typically specify rent amount, late fees, and security deposits subject to legal limits, along with operational house rules covering kitchen use, quiet hours, and parking. The American Association of Landlords provides a California-specific lease template that addresses the unique shared-space dynamics of ADU rentals.

House rules matter more in ADU settings than in standard rentals because the owner often lives on the same property. Clear rules about guest policies, shared outdoor spaces, trash pickup, and noise reduce friction before it starts. Ambiguity in lease terms is the leading cause of tenant disputes in owner-occupied rental situations.

- Define shared spaces explicitly. Specify which outdoor areas, laundry facilities, or storage spaces the tenant may use.

- Set quiet hours in writing. A clause covering noise between 10:00 PM and 7:00 AM prevents the most common neighbor complaints.

- Cap long-term guests. A guest policy limiting stays beyond 14 consecutive days protects against unauthorized occupants.

- Use automatic rent increases. A CPI-linked annual increase clause keeps rent aligned with the market without requiring lease renegotiation.

Pro Tip: Tenant turnover is the biggest hidden cost in ADU rentals. A tenant who stays three years costs far less in vacancy and re-leasing fees than three tenants in the same period. Price rent slightly below peak market to attract long-term renters.

Effective tenant management reduces vacancy, cuts turnover costs, and stabilizes annual income. Legal compliance and clear lease agreements work together to minimize disputes and keep the unit occupied. The combination of a solid lease, clear house rules, and responsive management is what converts theoretical rental income into actual cash in your account.

Key Takeaways

ADU rental income potential is real and financially significant, but it is bounded by Fannie Mae’s 30% qualifying income cap, legal permitting requirements, and the quality of your lease and management practices.

| Point | Details |

|---|---|

| 30% qualifying income cap | Fannie Mae limits ADU rent to 30% of total qualifying income under DU v12.1 rules. |

| Legal permitting is non-negotiable | Unpermitted ADUs generate no lender-recognized income and create financing and legal risk. |

| Market rent benchmarks exist | A 1-bedroom ADU in Fresno averages $1,323/month at 96% occupancy, a useful baseline. |

| Comps must match the unit | Freddie Mac requires at least three comparable rentals, including one rented ADU. |

| Lease quality drives stability | Clear lease terms and house rules reduce turnover and protect realized income. |

ADU income is a business line, not a windfall

I have seen homeowners build beautiful ADUs and then model the income based on the highest rent they found on a quick online search. That approach fails almost every time. The unit sits vacant for two months because the rent is $300 above market. The owner drops the price, loses the first month’s income, and then wonders why the numbers do not pencil out.

The right mental model is to treat ADU income like a small business line attached to your home. Small businesses do not assume 100% revenue every month. They budget for slow periods, set prices based on real market data, and build systems that reduce operating friction. That same discipline applied to an ADU produces consistent, predictable income rather than a frustrating cycle of optimism and disappointment.

The 2026 Fannie Mae rules are actually a useful forcing function. The 30% qualifying income cap forces you to think conservatively from the start. If your ADU income cannot move the needle within that cap, the unit still adds property value and cash flow. It just does not transform your mortgage qualification the way some online calculators suggest. Engage a lender early, get a proper appraisal, and build your income model on real comps, not wishful thinking. That approach produces results you can count on.

— Rudy

Live Large™ resources for ADU policy and rental income planning

Live Large™ works with homeowners and investors at every stage of ADU development, from design and permitting through construction and financing. If you are evaluating rental income potential in a specific market, understanding local policy changes is the right starting point.

Florida and the Tampa Bay region are seeing significant ADU policy shifts that directly affect rental income opportunities. Live Large™ covers Tampa’s ADU policy reforms in detail, including how zoning changes affect what you can build and rent. For homeowners in Pasco County, Live Large™ also tracks Pasco County’s ADU approvals and what they mean for rental income potential in that market. Use these resources to stay current on the regulatory environment before you commit to a development plan.

FAQ

What is the Fannie Mae 30% cap on ADU rental income?

Fannie Mae limits ADU rental income to 30% of total qualifying income under Desktop Underwriter v12.1, effective march 21, 2026. This cap applies to both purchase and limited cash-out refinance transactions on one-unit principal residences.

Does an unpermitted ADU count toward rental income for financing?

No. Lenders and appraisers do not recognize income from unpermitted ADUs. Only legally permitted units with documented rental history and market-supported appraisals qualify for lender-accepted income calculations.

How many rental comps does Freddie Mac require for ADU income?

Freddie Mac requires at least three comparable rentals, including at least one rented ADU, to support the income figure used in appraisal and financing. Comps must match the unit’s type, privacy level, and location.

What does a typical ADU rent for in a mid-size California market?

A 1-bedroom ADU in Fresno County rents for approximately $1,323 per month at 96% occupancy, producing roughly $15,241 in gross annual rent and a 6.5% cap rate. Rents vary by unit type, finish level, and proximity to employment centers.

What should an ADU lease agreement include?

An effective ADU lease agreement specifies rent amount, late fees, security deposit terms, and house rules covering quiet hours, guest limits, shared space use, and parking. California-specific templates from organizations like the American Association of Landlords address the unique dynamics of owner-occupied ADU rentals.